On April 13, 2023 a local newspaper ran an article on my class with the following headline

This is a bold headline but one I stand by so lets break it down and examine the series of posters that goes with this headline.

Teaching young people is hard. Their phone gives them instant access to everything so I figured this headline might get their attention and I was right. I put this poster in the hallway outside my classroom and it is a great conversation starter with kids. I also have versions of this poster in my classroom to remind my personal finance students of what they are working towards.

I really want all students to make this their reality so I give them the instructions.

Here is how it works.

Step 1: Open a Roth IRA at Fidelity and deposit $500 a month. If you cannot make $500 a month work, then invest whatever you can and work towards $500/month. The minimum amount with Fidelity is $10 a month.

Step 2: Buy an ETF (exchange traded fund) that tracks the S&P500. This could be SPY, VOO or IVV.

Step 3: Every month deposit $500 and buy SPY, VOO or IVV.

Step 4: Repeat Step 3 for 40 years.

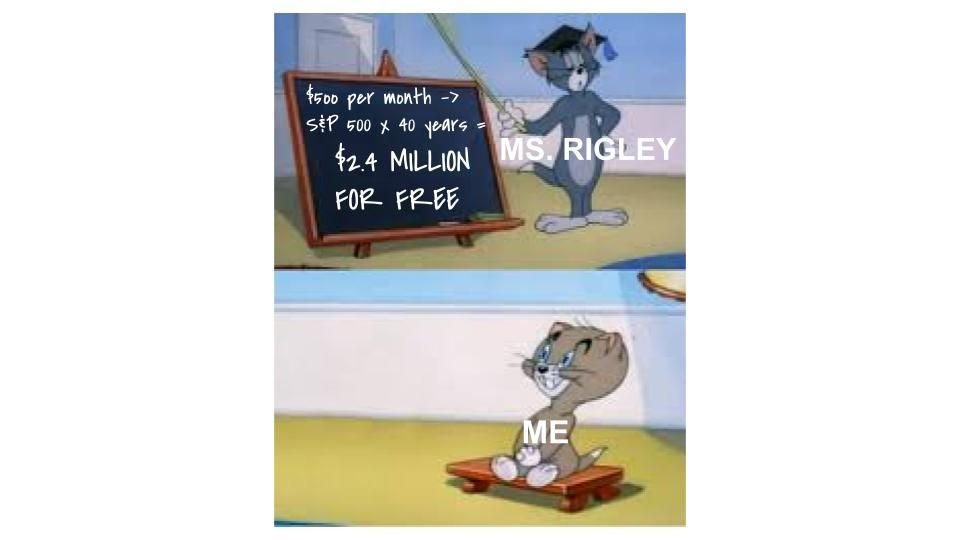

The thing about this - it has to be 40 years!!!! Take it out 5 years earlier and you lose $1,000,000!

Time is the secret sauce to this magic. Over the course of 40 years, you turned $240,000 into $2,655,555. Hence a free $2,415,555.

This equation assumes a rate of return of 10% which is the historical average of the S&P 500. No, this does not account for inflation but inflation is going to happen regardless so you might as well get investing.

Ultimately, students might need more than this but I don’t want to scare them so this is where we start. In my Personal Finance class we talk about the financial freedom calculation [Yearly expenses x 25 = their financial freedom number] and the fact that they may have to adjust their investments as their life circumstances change. It is estimated that you can withdraw 4% of your account each year and not run out of money which would give them $106,222 annually. In 40 years, this might be more like $50,000 or less which may or may not be enough depending on their circumstances. Review my blog post about financial freedom.

Disclaimer: I am an educator, not your personal financial advisor. Please make sure to do your own research before moving forward with any actions discussed in this newsletter.

Know that all investments involve some form of risk and there is no guarantee that you will be successful in making, saving, or investing money; nor is there any guarantee that you won’t experience any loss when investing. Past performance does not guarantee future performance. Always remember to make smart decisions and do your own research!